Use the following to answer question:

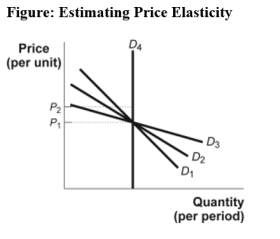

-(Figure: Estimating Price Elasticity) Use Figure: Estimating Price Elasticity.Between the two prices,P1 and P2,which demand curve has the LOWEST price elasticity?

Definitions:

Long-Run Equilibrium

A state in which all inputs are variable, enabling firms to make adjustments to output and prices to reach a point where no firm desires to change its production or exit the market.

Increasing Cost Industry

An industry in which production costs increase as output expands, often due to limited resources or other constraints.

Increasing-Cost Industry

An industry in which the costs of production increase as more firms enter the market, typically due to limitations in resources.

Decreasing-Cost Industry

An industry in which the average cost of production decreases as the industry grows and output increases.

Q26: If the elasticity of demand is _

Q49: Suppose Governor Meridias decides to initiate a

Q69: Paying a tax of $20 on an

Q140: If total revenue goes up when the

Q162: A tax system _ when taxes are

Q188: The price elasticity of demand for a

Q202: If two goods are substitutes,their cross-price elasticity

Q229: An excise tax is levied on suppliers.The

Q240: (Figure: Tax Incidence)Use Figure: Tax Incidence.Consumers are

Q251: A tariff or quota will _ prices