Use the following to answer question:

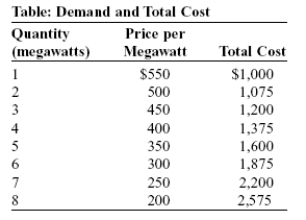

-(Table: Demand and Total Cost) Use Table: Demand and Total Cost.Lenoia runs a natural monopoly firm producing electricity for a small mountain village.The table shows Lenoia's demand and total cost of producing electricity.The maximum profit Lenoia can make is:

Definitions:

Increasing Cost Industry

An industry in which costs of production increase as firms enter the market, often due to limited resources or factors of production becoming more expensive.

Long-Run Supply Curve

A graphical representation that shows how the quantity supplied reacts to price changes in the long-term, accounting for all factors of production adjustments.

Increasing Cost Industry

An industry in which the costs of production increase as the industry's output expands, typically due to resource limitations.

Decreasing-Cost Industry

An industry where the average cost of production decreases as the industry's output increases, often due to economies of scale.

Q84: (Figure: Short-Run Costs)Use Figure: Short-Run Costs.This firm's

Q106: (Figure: The Profit-Maximizing Firm in the Short

Q110: The practice of one company tacitly setting

Q138: In perfect competition,the firm produces the output

Q183: Gary's Gas and Frank's Fuel are the

Q192: Until recently,most advanced countries except the United

Q217: In perfect competition:<br>A)a firm's total revenue is

Q220: Goods that are subject to network externalities

Q220: (Figure: The Profit-Maximizing Firm in the Short

Q282: (Figure: The Profit-Maximizing Output and Price)Use Figure: