Use the table below to answer the following questions.

Table 11.2.1

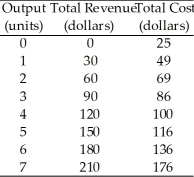

-Refer to Table 11.2.1,which gives the total revenue schedule and total cost schedule of a perfectly competitive firm.If the firm produces 2 units of output,it

Definitions:

Real Cost

The total cost of producing a good or service, including all resources consumed and opportunity costs, in contrast to its financial cost.

Law of Diminishing Returns

An economic principle stating that as investment in a particular area increases, the rate of profit from that investment, after a certain point, cannot continue to increase if other factors remain constant.

LRATC

Long-Run Average Total Cost, referring to the average cost per unit of output when all inputs are considered variable over time.

Economies of Scale

Businesses experience cost savings linked to the size of their operations, with the per-unit cost usually falling as the operation size grows.

Q10: Initially,a perfectly competitive market that has 1,000

Q21: If income decreases,the budget line<br>A)becomes steeper.<br>B)becomes flatter.<br>C)shifts

Q24: A contestable market exists whenever<br>A)two or more

Q43: The budget line depends on<br>A)income only.<br>B)prices only.<br>C)income

Q48: Because consumers value product variety,<br>A)the demand for

Q49: Peter's income increases and so does his

Q51: Refer to Table 13.1.1.The four-firm concentration ratio

Q96: Refer to Figure 15.3.3.The figure shows the

Q103: If firms in a perfectly competitive market

Q110: Refer to Table 11.1.1 which gives the