Use the following to answer question(s) : Demand, Elasticity, and Total Revenue

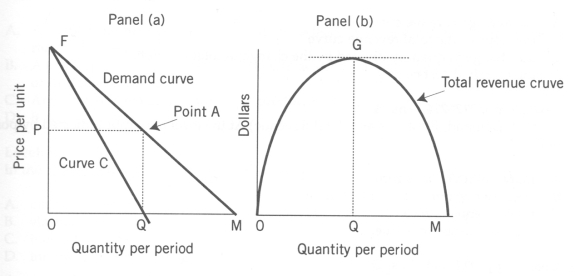

-(Exhibit: Demand, Elasticity, and Total Revenue) When price is P and quantity is Q in Panel (a) , which of the following is (are) true?

Definitions:

Economic Analysis

A methodical strategy for deciding the best way to allocate limited resources, which includes evaluating multiple options to reach a particular goal within established assumptions and limitations.

Marginal Changes

Marginal changes describe small adjustments to a variable's quantity or level, analyzing the effects of these adjustments on an overall system.

Status Quo

The existing state or condition of affairs, often used in the context of maintaining current circumstances without change.

Entrepreneurship

The act of creating, organizing, and running a new business venture to take advantage of market opportunities, often involving risk and innovation.

Q11: (Exhibit: Firms in Monopolistic Competition) Negative economic

Q22: (Exhibit: Short-Run Monopoly) The profit-maximizing rule is

Q25: If demand is elastic and price falls,

Q58: The main characteristic that distinguishes monopolistic competition

Q101: Beyond some point a higher wage may

Q111: The Case in Point on hockey teams

Q136: A monopoly responds to an increase in

Q138: Total cost is equal to the quantity

Q152: Marginal revenue product is the:<br>A) change in

Q172: An increase in the participation of women