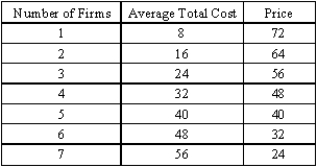

The following relationship between price, average total cost, and the number of firms describes an industry in a single country.  (A)Graph the relationship between average total cost and the number of firms, as well as the relationship between price and the number of firms.

(A)Graph the relationship between average total cost and the number of firms, as well as the relationship between price and the number of firms.

(B)Find the long-run equilibrium price and number of firms.

(C)Suppose the country opens to trade with other countries. Which line will shift and in which direction? What will happen to the long-run equilibrium price and the number of firms in the industry?

Definitions:

Marginal Cost Curve

A graphical representation showing how the cost to produce one additional unit changes as more units are produced.

Long-Run Supply

A period sufficient for all inputs to production, including capital, to be varied, allowing for adjustments to changes in demand or technology.

Average Total Cost

The total cost of production divided by the total quantity produced, representing the per-unit cost of production.

Long-Run Equilibrium

A state in which all factors of production and economic variables are in balance, with no external pressures forcing change.

Q44: An appreciation of Mexico's peso<br>A) decreases Mexican

Q54: Refer to Exhibit 30-1. If the importing

Q64: The U.S. government did not intervene to

Q73: The possible return on an uncertain investment

Q93: A developing country refers to a country

Q95: The Case in Point on the Simpsons

Q112: The economic way of thinking includes:<br>A) more

Q143: A wise development strategy would be to

Q184: The effect the Smoot-Hawley tariff had on

Q192: There are winners and losers as a