Refer to the information provided in Figure 28.7 below to answer the question(s) that follow.  Figure 28.7

Figure 28.7

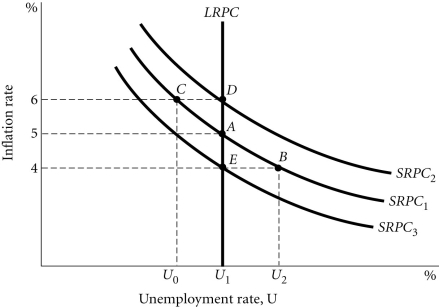

-Refer to Figure 28.7. Suppose the economy is at Point A, and the cost of inputs is fixed. An increase in government spending could move the economy to Point

Definitions:

Technological Change

The process of innovation and development of new methods, products, or processes, driving efficiency and economic growth.

Fixed Costs

Costs that do not vary with the level of production or sales, such as rent, salaries, and insurance, making them consistent regardless of business activity levels.

Short Run

A period of time in which at least one input, such as plant size, is fixed and cannot be changed by the firm, limiting its capacity to adjust output levels.

MC = P

A condition in economic theory where Marginal Cost (MC) equals Price (P), indicating optimal production levels where no additional units should be produced.

Q27: Refer to Figure 29.2. The price will

Q75: The minimum wage law contributes to a<br>A)

Q154: If productivity increases as wages increase and

Q162: If wages are sticky, a decrease in

Q165: An increase in aggregate demand when the

Q167: A decrease in government spending shifts aggregate

Q181: Refer to Figure 28.6. Assuming all shocks

Q185: For an economy to experience both economic

Q209: At the end of 2014, the economy

Q272: A vertical aggregate supply curve implies a