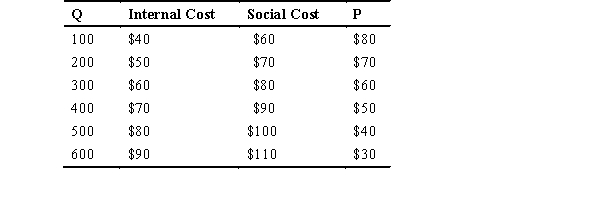

Refer to the accompanying table,where Q represents the quantity produced,internal cost and social cost are given for various quantities,and P represents the price consumers are willing to pay for various quantities,to answer the following questions.

-The market equilibrium occurs where price is ________ and quantity is ________.

Definitions:

Applied Overhead

The amount of factory overhead costs allocated to individual units of production, based on a predetermined rate.

Actual Overhead

The real expenses incurred during a period for indirect costs, differing from budgeted or estimated overhead.

Schedule of Cost

A detailed report or document that itemizes and categorizes the various costs associated with a project or production, often used for budgeting and financial analysis.

Job Costing System

An accounting method used to assign costs to specific jobs or projects, tracking expenses to assess profitability.

Q6: If the market price of a product

Q15: The deadweight loss from a tax is

Q40: Which graph would result in firms exiting

Q82: What three incentives commonly exist for people

Q86: Compare and contrast natural barriers to entry

Q91: Imagine you find yourself in a heat

Q101: What is the total amount of producer

Q102: The government oversight and management of monopolies<br>A)

Q125: To reduce the level of pollution emitted

Q139: The change in total cost given a