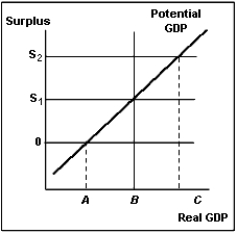

Exhibit 26-1

-If real GDP equals C in Exhibit 26-1,

Definitions:

Increasing-cost Industry

An industry in which the costs of production increase as the industry expands due to factors like limited resources or higher input prices.

Long-run Supply

The time period in economics during which all factors of production and costs are variable, allowing firms to adjust all inputs in response to market conditions.

Supply Curve

A graphical representation showing the relationship between the price of a good and the quantity of the good that suppliers are willing to produce and sell.

Decreasing-cost Industry

An industry where costs per unit decline as the industry's output increases due to economies of scale.

Q1: The leftward shift of the AD curve

Q2: An important precondition that enables a country

Q6: Discuss the difference in the short-run and

Q24: Economists refer to the sum of all

Q33: Explain the relationship between the intersection of

Q92: What justifies the proposition that China is

Q118: In the economic fluctuations model, the so-called

Q141: Which of the following statements about the

Q150: A macroeconomic theory that stresses the fact

Q165: Which of the following is the best