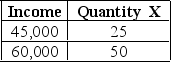

Given the following income and quantity demanded for good X, we know that this good is a superior good.

Definitions:

Marginal Cost Curve

A graph showing how the cost of producing one more unit of a good varies as the quantity of production increases.

Short Run

in economics, refers to a period during which at least one factor of production is fixed, and firms can adjust only the variable factors.

TVC

Total Variable Cost, which refers to all variable expenses that change with the level of output.

Short Run

A period of time in economics during which at least one input is fixed, limiting the ability of the economy or firm to adjust.

Q3: Isaac knows there are two other firms

Q3: Fill out the following table and find

Q14: The following table is for two martial

Q26: Perfect competition most closely refers to a:<br>A)

Q38: In the long run, because of the

Q38: "If you were designing a company to

Q42: Variable costs are costs that increase as

Q46: Price rigidity refers to the inability for

Q51: Market conditions for the perfectly competitive firm

Q72: The kinked demand curve model assumes that