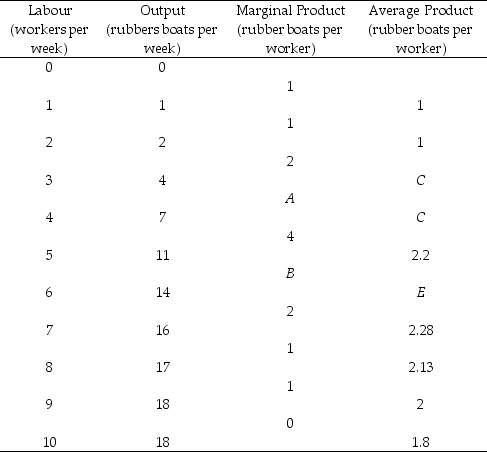

Use the table below to answer the following questions.

Table 11.2.3

-Refer to Table 11.2.3. The maximum value of marginal product occurs where output equals ________, while the maximum value of average product occurs where output equals ________.

Definitions:

Price Elasticity

A measure of how much the quantity demanded of a good responds to a change in its price.

Quantity Sold

The total number of units of a product or service that have been purchased in a given period.

Price Elasticity

A measure of how much the quantity demanded or supplied of a good changes in response to a change in its price.

Demand Curve

A visual chart that illustrates how the quantity of a product or service desired by buyers varies with its price.

Q2: Technological change spreads through a perfectly competitive

Q13: Consider a monopolistically competitive industry which is

Q16: What is a distinguishing characteristic of goods

Q40: Which one of the following statements is

Q76: A firm with one or more owners

Q84: In monopolistic competition,advertising costs<br>A)are fixed costs.<br>B)can result

Q88: Refer to Figure 9.1.2.Which budget line has

Q96: Marginal utility theory predicts that a rise

Q98: Under monopolistic competition,long-run economic profit is zero

Q100: Let Y = $100,Q<sub>X</sub> = quantity of