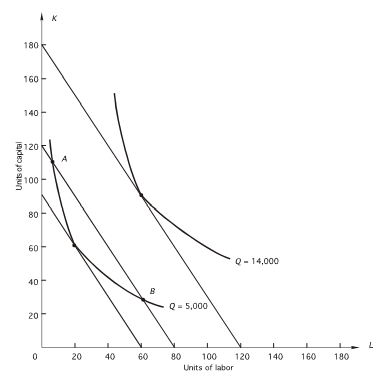

Refer to the following graph.The price of capital (r) is $20.  What is the lowest possible cost at which 14,000 units of output can be produced?

What is the lowest possible cost at which 14,000 units of output can be produced?

Definitions:

Decrease in Price

A reduction in the cost at which goods or services are sold, often leading to increased demand.

Increase in Quantity

A rise in the amount of goods or services produced or supplied.

Market Equilibrium

The state in which market supply and demand balance each other, leading to stable prices.

Prices of Resources

Refers to the cost associated with the inputs required for production, including labor, capital, and materials.

Q17: When marginal revenue is zero,<br>A)P < MR.<br>B)P

Q30: A firm is making production plans

Q48: estimated demand for a good is

Q51: out the table and answer the

Q52: A firm sells its product to two

Q54: Refer to the following graph.The price of

Q55: A firm sells two goods (X

Q55: Given the table below,as the number

Q75: A radio manufacturer is experiencing theft

Q96: Which of the following is NOT a