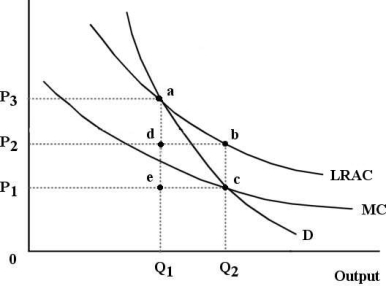

The diagram below shows the market demand curve and the cost curves for a single firm.

FIGURE 12-6

FIGURE 12-6

-Refer to Figure 12-6.Suppose this firm is being regulated using a policy of average -cost pricing.In this case,economic profits to the firm are represented by the area

Definitions:

Long-Run Equilibrium

A state in which all factors of production and inputs can be adjusted by firms, leading to a situation where no firm has an incentive to change its output or production method.

LRAC Curve

Long-Run Average Cost Curve, a graphical representation showing the minimum cost at which any output level can be produced in the long run.

Exiting Firms

Businesses that are leaving a particular market due to various reasons such as unprofitability, strategic realignment, or market saturation.

Increasing-Cost Industry

An industry in which production costs increase as the industry's output expands.

Q12: Suppose there are only five construction companies

Q18: Suppose that in a perfectly competitive industry,

Q54: Refer to Figure 12-3. The area representing

Q57: An oligopolistic firm often detects a change

Q63: Refer to Figure 13-1. Suppose this firm

Q78: The fact that it is difficult to

Q84: Refer to Figure 11-2. A perfectly competitive

Q98: Monopolistic competition is similar to perfect competition

Q104: Assume a firm is using 10 units

Q117: In the long run it is not