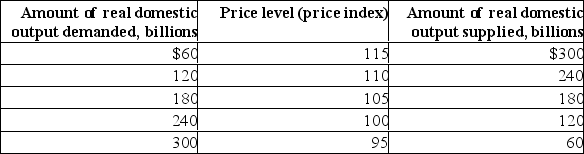

Suppose the aggregate demand and short-run aggregate supply schedules for a hypothetical economy are as shown below:

(a) What will be the equilibrium price and real output level in this hypothetical economy? Is this level of real GDP also the full-employment level of output? Explain.(b) Why won't a price level of 100 be the equilibrium price level? Why won't a price level of 110 index be the equilibrium price level?

(a) What will be the equilibrium price and real output level in this hypothetical economy? Is this level of real GDP also the full-employment level of output? Explain.(b) Why won't a price level of 100 be the equilibrium price level? Why won't a price level of 110 index be the equilibrium price level?

(c) Suppose aggregate demand increases by $120 billion at each price level.What will be the new equilibrium price and output levels?

(d) What factors might cause aggregate demand to increase?

(e) Suppose short-run aggregate supply increases by $120 billion at each price level.What will be the new equilibrium price and output levels?

Definitions:

Marginal Product

The additional output produced by using one more unit of a given input, holding all other inputs constant.

Marginal Cost Curve

A graphical representation that shows how the cost of producing one additional unit of a good changes as the production volume varies.

Short-Run Marginal Cost

The change in total cost associated with producing one additional unit of output, considering some inputs are fixed.

Embryonic Disk

A key structure in early embryonic development from which the embryo begins to form.

Q14: Which types of industries are hit hardest

Q19: Answer the next five questions on the

Q22: Define worker-hours and labour productivity.What factors are

Q25: What determines the equilibrium price level and

Q32: Keynes developed his theory during the height

Q36: Why might trade barriers be a highly

Q53: How does deterioration in the quality of

Q117: According to the application, oil prices in

Q244: As used in economics, the notion of

Q261: (The following economy produces two products.) Production