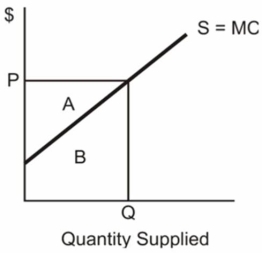

Draw a market supply curve and indicate the following:

(a) The market price;

(b) The quantity supplied;

(c) The minimum amount that sellers are willing to accept for the quantity supplied;

(d) The actual amount that sellers receive for providing the quantity supplied;

(e) The producer surplus from providing the quantity supplied.

Definitions:

Tax Revenue

The earnings collected by governments via tax imposition.

State Income Tax

A tax levied on income by some states, where the tax rate can vary by state and is applied to income earned by residents and sometimes nonresidents working in the state.

Highway Spending

Government expenditure on the construction and maintenance of road infrastructure, which is crucial for economic development, transportation efficiency, and public safety.

Administrative Burden

The costs associated with regulatory compliance, paperwork, and bureaucratic procedures that organizations must bear.

Q9: Supply in a market is represented by

Q10: What is the long-run equilibrium in the

Q12: At the current level of real GDP,<br>Sa

Q15: (a) Determine the equilibrium price and quantity

Q15: Compare the Uniform Crime Reports (UCR) with

Q18: List nine characteristics of the market system.

Q37: Evaluate this argument for a trade barrier:

Q40: Describe and explain the specter of deflation.

Q41: According to Richard A. Cloward and Lloyd

Q76: Which of the following is true of