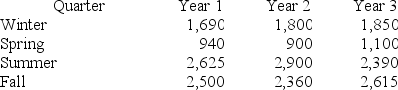

Consider the following set of quarterly sales data, given in thousands of dollars.

The following dummy variable model that incorporates a linear trend and constant seasonal variation was used: y(t) = β0 + β1t + βQ1(Q1) + βQ2(Q2) + βQ3(Q3) + Et. In this model, there are three binary seasonal variables (Q1, Q2, and Q3), where Qi is a binary (0,1) variable defined as:

The following dummy variable model that incorporates a linear trend and constant seasonal variation was used: y(t) = β0 + β1t + βQ1(Q1) + βQ2(Q2) + βQ3(Q3) + Et. In this model, there are three binary seasonal variables (Q1, Q2, and Q3), where Qi is a binary (0,1) variable defined as:

Qi = 1, if the time series data is associated with quarter i;

Qi = 0, if the time series data is not associated with quarter i.

The results associated with this data and model are given in the following Minitab computer output.

The regression equation is

Sales = 2442 + 6.2 Time − 693 Q1 − 1499 Q2 + 153 Q3

Analysis of Variance

Analysis of Variance

At α = .05, test the significance of the model.

At α = .05, test the significance of the model.

Definitions:

Aggressor

A person or entity that initiates hostility or attack, whether physical or psychological, against others.

Dominator

An entity or individual that exercises control or exert supremacy over others in a commanding or dominating manner.

Modeled Behavior

Actions displayed by an individual that serve as a reference for others, potentially influencing their behavior through observation and imitation.

Using Praise

The act of expressing approval or admiration to encourage or reinforce positive behavior or achievements.

Q13: In the past, of all the students

Q22: The effect of both repressors and activators

Q25: A local tire dealer wants to predict

Q28: An experiment was performed on a certain

Q34: The following frequency table summarizes the ages

Q45: Based on 25 time-ordered observations from a

Q52: A corn farmer has categorized the weather

Q53: When the quadratic regression model y =

Q60: A single-layer perceptron neural network model consists

Q124: Those fluctuations that are associated with climate,