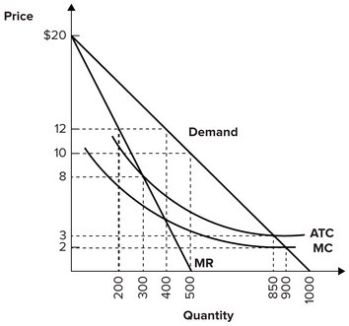

Refer to the graph shown. If this monopolist were forced to set price equal to marginal cost, in the long run it probably would:

Definitions:

Long-Run Cost Function

A graphical or mathematical representation that shows the lowest cost at which a firm can produce any given level of output in the long run, when all inputs are variable.

Positive Output

A situation where the production of goods or services is above zero.

Production Function

An equation or system that illustrates the connection between production inputs and the resulting products or services.

Long-Run Total Cost

Refers to the total cost incurred by a firm in producing a given output when all inputs, including both fixed and variable costs, are considered over a longer period.

Q25: A profit-maximizing monopolist will always set price

Q74: Which of the following is most likely

Q100: The underclass in the United States has

Q104: Refer to the graph shown. The welfare

Q106: Refer to the graph shown depicting a

Q106: Each firm in perfect competition:<br>A) sets quantity

Q133: The price at which a monopolistically competitive

Q135: Marginal product eventually:<br>A) declines because some inputs

Q199: Because a monopolistic competitor has some monopoly

Q202: Refer to the graph shown depicting a