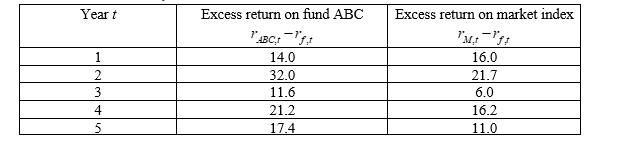

Suppose you have 5-year annual data on the excess returns on a fund manager’s portfolio (“fund ABC”) and the excess returns on a market index (where  is the return on fund ABC,

is the return on fund ABC,  is the risk-free rate and

is the risk-free rate and  is the return on the market index) :

is the return on the market index) :

-Suppose that the unbiased estimator of the standard deviation of the disturbance (s) is 5.1. What is the nearest value to the standard errors of the estimated CAPM alpha (  ) of Fund ABC from question 6?

) of Fund ABC from question 6?

Definitions:

Managements' Discussion

A section of a company's annual report where management provides an analysis of the company's financial condition and operational results.

Altman's Z-Score

A formula used to predict the likelihood of a business entering bankruptcy within two years, based on various income and balance sheet values.

Bankruptcy Risk

The risk that a company will be unable to meet its debt obligations and forced to seek protection under bankruptcy laws.

Default Risk

The risk that a borrower will not make the required payments on its debt obligations.

Q5: Which of the following statement is true

Q9: A Markov process can be written mathematically

Q10: Suppose that we wanted to sum the

Q14: The method of estimating econometric models which

Q17: All groups are teams, but not all

Q27: The linear relationship between two variables (y

Q41: An individual who is typically irritable, aggressive,

Q47: An intellectual characteristic of creative people is

Q55: Team leader Steve wants to personally observe

Q60: Laura always scores extremely high on conscientiousness.