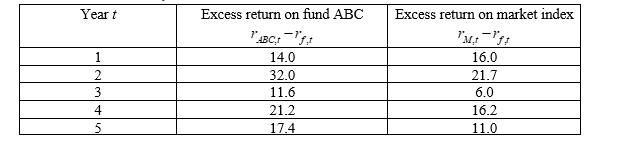

Suppose you have 5-year annual data on the excess returns on a fund manager’s portfolio (“fund ABC”) and the excess returns on a market index (where  is the return on fund ABC,

is the return on fund ABC,  is the risk-free rate and

is the risk-free rate and  is the return on the market index) :

is the return on the market index) :

-What is the most appropriate interpretation of the assumption concerning the regression disturbance terms?

Definitions:

Independent Directors

Board members who do not have a material or pecuniary relationship with the company or its related parties, except for board compensation, ensuring unbiased and objective decisions.

Audit Committees

A subgroup of a company's board of directors responsible for overseeing financial reporting and disclosure.

Profit Maximization

The process by which a firm determines the price and output level that returns the greatest profit.

Deontological Theory

A moral philosophy that emphasizes the importance of duty and the inherent morality of actions, rather than outcomes or consequences.

Q11: A major listening problem many leaders face

Q23: Given the data in question 6, what

Q28: Leadership development can take place by using

Q40: A company with a strategy of high

Q46: What label describes personality that is both

Q52: Charlie just broke up with his boyfriend

Q63: Emotional stability<br>A)Disinhibition<br>B)Detachment<br>C)Negative affectivity<br>D)Antagonism<br>

Q63: Anxious-ambivalent attachment style<br>A)Someone who worries that other

Q72: A major criteria for personality disorders is

Q84: Across a wide variety of cultures, _