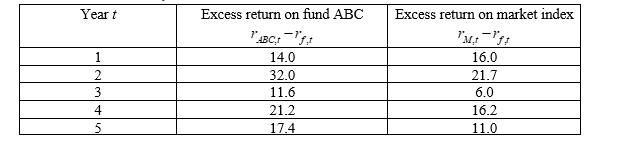

Suppose you have 5-year annual data on the excess returns on a fund manager’s portfolio (“fund ABC”) and the excess returns on a market index (where  is the return on fund ABC,

is the return on fund ABC,  is the risk-free rate and

is the risk-free rate and  is the return on the market index) :

is the return on the market index) :

-The estimators  and

and  determined by OLS will be the Best Linear Unbiased Estimators (BLUE) if which of the following assumptions hold?

determined by OLS will be the Best Linear Unbiased Estimators (BLUE) if which of the following assumptions hold?

(I) The errors have zero mean

(II) The variance of the errors is constant and finite over all values of the independent variable(s)

(III) The errors are linearly independent of one another

(IV) There is no relationship between the error and corresponding independent variables

Definitions:

Controller

An executive role responsible for overseeing the accounting operations within a company, managing financial reporting, budgets, and internal controls.

Dissemination

The process of distributing or spreading information, knowledge, or data widely, especially to ensure accessibility to relevant stakeholders.

Operating Cycle

The duration between the acquisition of inventory and the collection of cash from receivables.

Cash Cycle

The time period it takes for a company to convert its investments in inventory back into cash, through sales.

Q2: Consider the following matrix: <sub> </sub> <img

Q16: Integrity tests typically measure all of the

Q26: The central limit theorem states that<br>A) The

Q31: A sign of possible misunderstanding when communicating

Q35: Bethany often has emotional outbursts for no

Q37: Randy is participating in the strange situation.

Q38: John is the newly appointed managing director

Q52: Planning is not the only important component

Q62: Katie is anxious. There is likely a

Q63: Funder is researching how extraversion and openness