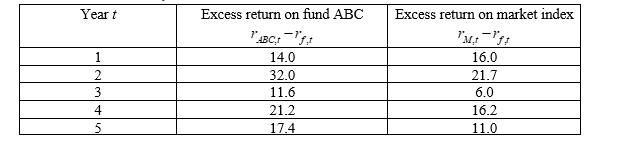

Suppose you have 5-year annual data on the excess returns on a fund manager’s portfolio (“fund ABC”) and the excess returns on a market index (where  is the return on fund ABC,

is the return on fund ABC,  is the risk-free rate and

is the risk-free rate and  is the return on the market index) :

is the return on the market index) :

-Suppose that the unbiased estimator of the standard deviation of the disturbance (s) is 5.1. What is the nearest value to the standard errors of the estimated CAPM alpha (  ) of Fund ABC from question 6?

) of Fund ABC from question 6?

Definitions:

EPS

Earnings Per Share, a financial metric that divides a company's profit by the number of its shares outstanding.

Market Capitalization Rate

The expected return on an investment in a market portfolio, based on the market price of risk.

Constant-Growth DDM

A model for valuing a company's stock by using predicted dividends and discounting them back to present value assuming a constant growth rate.

Preferred Share

A class of ownership in a corporation with a higher claim on assets and earnings than common stock.

Q5: Self-schemas can be useful for acquiring information,

Q10: Volatility clustering is<br>A) The tendency for financial

Q10: Research on workgroups suggests that groups composed

Q18: Which of the following statements is

Q19: Self-efficacy is an important part of our

Q38: An important way for leaders to capitalize

Q41: Which partner in a heterosexual relationship would

Q54: Ryan's team has performed beyond the performance

Q58: Which of the following is a characteristic

Q88: According to the text, labeling personality disorders