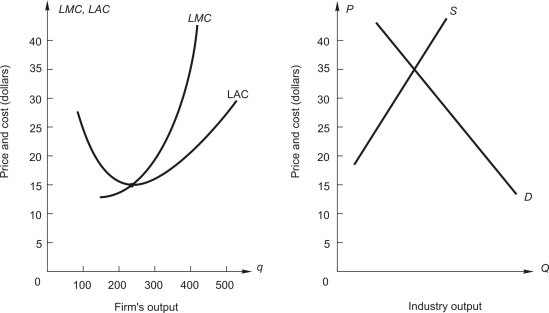

Refer to the following figure:

The graph on the left shows long-run average and marginal cost for a typical firm in a perfectly competitive industry. The graph on the right shows demand and long-run supply for an increasing-cost industry.

-If this were an increasing cost industry, what would be the price when the industry gets to long-run competitive equilibrium?

Definitions:

Relatively Elastic

Refers to a situation where the quantity demanded or supplied of a good changes significantly in response to changes in price.

Percentage Increase

calculates the rate at which a quantity grows over a period, expressed as a fraction of its original value.

Elastic

Describes a scenario where a small change in price leads to a large change in quantity demanded or supplied.

Inelastic

describes a situation where the demand or supply for a good is not significantly affected by changes in price.

Q12: How many units of X will the

Q18: The marginal cost function is:<br>A) SMC =

Q27: Suppose that 25 units of X and

Q36: What is the price per unit of

Q41: What is the new own price elasticity

Q42: Which of the follow is NOT a

Q46: A firm with market power<br>A) can increase

Q80: In the table above, what is the

Q91: How many units of labor should the

Q93: When the firm uses 120 units of