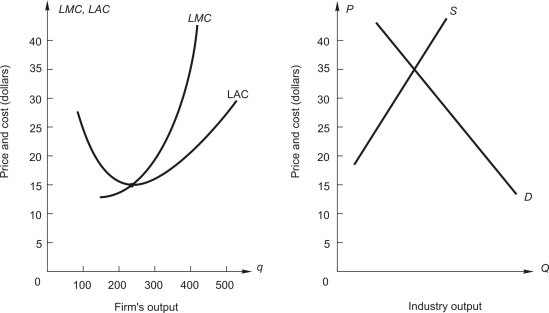

Refer to the following figure:

The graph on the left shows long-run average and marginal cost for a typical firm in a perfectly competitive industry. The graph on the right shows demand and long-run supply for an increasing-cost industry.

-If this were an increasing cost industry, what would be the price when the industry gets to long-run competitive equilibrium?

Definitions:

Mandated By Law

Requirements or actions that are legally imposed and regulated by legislation, which individuals or entities must comply with.

Host-Based Pay

Expatriate pay comparable to that earned by employees in a host country.

Skill-Based Pay

A compensation system that sets pay levels based on the skills or knowledge an employee possesses, rather than their job title or position.

Third-Country-Based Pay

A compensation strategy where an employee's pay is based on the standard of living and market rates in a country different from both the home and host countries.

Q1: What is the optimal price?<br>A) This is

Q8: If Greene Enterprises produces 6,000 units of

Q12: Suppose that market price is $2.60. A

Q21: If market price is $2, how much

Q41: _ is/are example(s) of market failure that

Q43: The minimum cost of producing 1,000 units

Q52: If the price elasticity of demand for

Q61: Suppose that when a firm increases output

Q61: How much does the 28th unit of

Q89: When the firm uses 4 units of