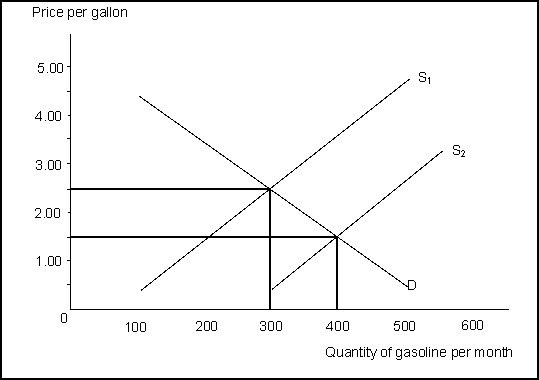

-(Exhibit: Demand and Supply of Gasoline) Given the equilibrium after a change in supply from S1 to S2:

Definitions:

Marginal Productivity Theory

An economic theory suggesting that payment to factors of production equals the value of their marginal contribution to the production process.

Equilibrium Value

The price at which the quantity of goods supplied is equal to the quantity of goods demanded in a market.

Factor Of Production

Inputs employed in the production of goods and services, typically classified as land, labor, capital, and occasionally entrepreneurship.

Average Product

The output per unit of input, such as labor or capital, used in the production process.

Q3: The law of increasing opportunity cost means

Q14: (Exhibit: Bicycles and Radishes 2)In the country

Q38: Whenever supply increases, the resulting market price

Q50: In enforcing the legal system, the government

Q51: There can be no shortages or surpluses

Q89: (Exhibit: The Demand for Bungalow Bob's Bagels)Demand

Q115: In a command socialist economy:<br>A)resources are government

Q125: The proposition that states that as output

Q166: The North Korean economy is currently classified

Q187: Suppose that the expected exam scores from