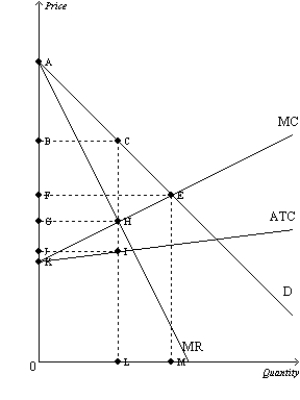

Figure 16-13

-Refer to Figure 16-13. What is the first step in this industry's adjustment to long run equilibrium?

Definitions:

Input Prices

The cost of resources used in the production process, including labor, materials, and capital.

Price Ceilings

Legal maximum prices set for particular goods and services, intended to protect consumers from very high prices.

Consumer Surplus

The variance between the actual cost paid by consumers and the maximum amount they're prepared to pay for a good or service.

Market Equilibrium

The point at which the quantity of a good or service demanded by consumers equals the quantity supplied by producers, resulting in a stable market price.

Q12: The market for novels is<br>A)perfectly competitive.<br>B)a monopoly.<br>C)monopolistically

Q281: Refer to Figure 16-11. If this firm

Q329: In the short run, a firm operating

Q365: A monopolistically competitive firm faces the following

Q372: Entry of new firms in monopolistically competitive

Q378: Because a monopolist must lower its price

Q399: A firm has the following cost structure:

Q432: Refer to Table 15-21. If the monopolist

Q489: At the profit-maximizing quantity of output for

Q566: Long-run profit earned by a monopolistically competitive