(Adapted from "Problem Eleven" from Chapter Six of previous editions of the textbook)

Alpha Ltd. is a Canadian-controlled private corporation operating a small land-development business 20x2, the company acquired a license to manufacture pre-fab homes and began operations immediate Financial information for the 20x2 taxation year is outlined below:

Alpha's profit before income taxes for the year ended November 30, 20x2, was $245,000, as follows:  The loss on sale of property results from two transactions. On October 1, 20x2, Alpha sold all of its s Ltd., a 100% subsidiary, for $100,000. (The shares were acquired seven years ago for $80,000.)Also the year, Alpha sold some of its vehicles for $25,000.The vehicles originally cost $50,000 and had a of $48,000 at the time of sale. New vehicles were obtained under a lease arrangement.

The loss on sale of property results from two transactions. On October 1, 20x2, Alpha sold all of its s Ltd., a 100% subsidiary, for $100,000. (The shares were acquired seven years ago for $80,000.)Also the year, Alpha sold some of its vehicles for $25,000.The vehicles originally cost $50,000 and had a of $48,000 at the time of sale. New vehicles were obtained under a lease arrangement.

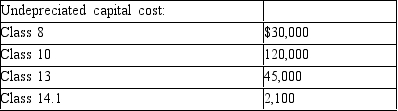

The 20x1 corporate tax return shows the following UCC balances:

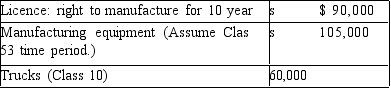

Alpha occupies leased premises under a seven-year lease agreement that began three years ago. At th Alpha spent $60,000 to improve the premises. The lease agreement gives Alpha the option to renew for two three-year periods. Alpha began manufacturing pre-fab homes on June 1, 20x2. At that time,

Alpha occupies leased premises under a seven-year lease agreement that began three years ago. At th Alpha spent $60,000 to improve the premises. The lease agreement gives Alpha the option to renew for two three-year periods. Alpha began manufacturing pre-fab homes on June 1, 20x2. At that time,

acquired the following:

Accounting amortization in 20x2 amounted to $60,000.

Accounting amortization in 20x2 amounted to $60,000.

Alpha normally acquires raw land, which it then develops into building lots for resale to individuals contractors. In 20x2, it sold part of its undeveloped land inventory to another developer for $400,000 realized a profit of $80,000, which is included in the land-development income above. The proceeds of $40,000 in cash, with the balance payable in five annual instalments beginning in 20x3.

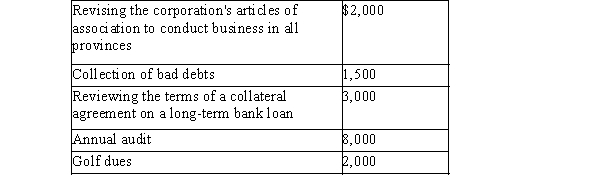

Travel and entertainment expense includes the following:  Legal and accounting expense includes the following:

Legal and accounting expense includes the following:  Required:

Required:

Calculate Alpha's net income for tax purposes for the 20x2 taxation year.

Definitions:

Markup Percent

The ratio by which the cost of a product is increased to arrive at its selling price, expressed as a percentage of the cost.

Travel Agent

A professional who arranges travel for individuals or groups, including accommodations, transportation, and itineraries.

Dollar Markup

The difference between the selling price of an item and its cost, expressed in dollar terms.

Water Color Paintings

A form of painting that uses pigments suspended in a water-based solution, often characterized by fluid and translucent layers.

Q4: Green Co. and Blue Co. are equal

Q12: A new water treatment operation is being

Q14: Two grandparents are considering purchasing a baby

Q21: What is an example of individual lifestyle

Q22: Consider the following cash flow. Determine

Q38: Cash dividends:<br>A)decrease revenue on the income statement.<br>B)decrease

Q43: Which of the following best describes a

Q68: Which of the following terms represents a

Q86: Revenues were $170,000, expenses were $90,000, and

Q98: Generally accepted accounting principles, or GAAP, are