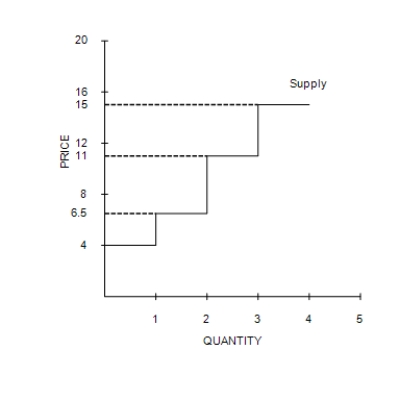

Figure 7-3

-Refer to Figure 7-3. If the price of the good is $13.00, then producer surplus is

Definitions:

Long-run Equilibrium Price

The price at which the quantity of a good demanded equals the quantity supplied, with all adjustments made for factors affecting supply or demand over time.

Product Demand

The desire and willingness of consumers to purchase a particular product at various prices during a certain period.

Purely Competitive Firm

A business functioning in an environment with numerous purchasers and vendors, where no single entity has the power to notably affect the prices in the market.

Technological Improvement

Advances and innovations in technology that enhance efficiency, productivity, or capabilities in various sectors.

Q4: Because the supply and demand of housing

Q29: Suppose the equilibrium price of a stick

Q112: A maximum amount that people have in

Q123: Suppose a freeze in Florida significantly reduces

Q123: Economists dismiss the idea that lower tax

Q135: Refer to Figure 6-19. If the government

Q164: A price ceiling set below the equilibrium

Q205: Producer surplus is the amount a seller

Q291: A tax on sellers increases supply.

Q311: Suppose buyers of protein shakes are required