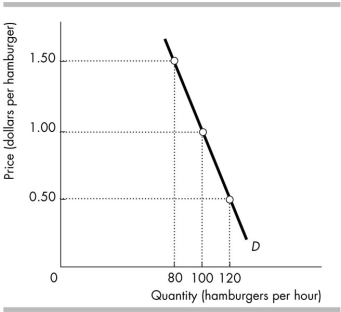

-The above figure illustrates the demand for hamburgers. When the price is $1 a hamburger, the elasticity of demand is _______ and a 1 per cent increase in the price will _______ the quantity of hamburgers demanded by _______ per cent.

Definitions:

Least Possible Cost

The minimum expenditure necessary to achieve a specific outcome or produce a given quantity of a good.

Input Markets

Marketplaces where firms buy resources, goods, and services necessary for producing their own products or services.

Output Markets

Markets where goods and services produced by businesses are sold to households, government entities, and other businesses.

General Equilibrium

A state in which all markets in an economy are in simultaneous equilibrium, taking into account the interactions between different markets.

Q12: Quotas and tariffs both<br>A) cause a loss

Q14: Which of the following will NOT shift

Q14: Value of marginal product equals marginal product<br>A)

Q51: Governments often intervene in agricultural markets by<br>A)

Q59: The demand curve in the figure above

Q71: In the above figure, when 2000 bicycles

Q99: The figure shows the market for books

Q106: Which of the following shifts the supply

Q110: The income elasticity of demand for bicycles

Q139: Which of the following statements is true?<br>A)