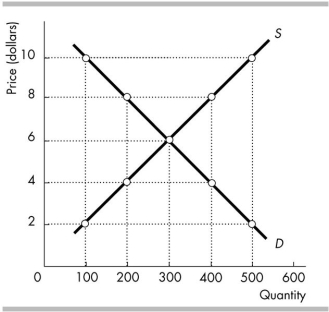

-In the above figure, the equilibrium price is _______ and the equilibrium quantity is _______.

Definitions:

Marginal Returns

The additional output that is produced by using one more unit of a given input, crucial in determining optimal production levels.

Total Fixed Costs

Expenses that do not change with the level of output or production in the short term, such as rent, salaries, and insurance.

Total Fixed Cost

The sum of all costs that remain constant regardless of the level of production or output within a given period.

Marginal Product of Labor

The additional output a firm gains by employing one more unit of labor, holding other inputs constant.

Q27: Demands differ from wants because<br>A) demands are

Q50: You observe that more labour is employed

Q73: In the above figure, a rent ceiling

Q79: The supply of lettuce in the short

Q92: Based on the above table, which of

Q94: In a bilateral monopoly, the wage rate

Q103: Adam makes $25,000 per year and Bob

Q115: Oscar and Felix are the only firms

Q121: In the figure above, if a minimum

Q146: If there is a collusive agreement in