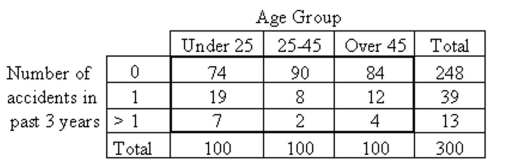

Determine the null and alternative hypotheses for the study that produced the data in the table.

-A car insurance company performed a study to determine whether an association exists between age and the frequency of car accidents. They obtained the following sample data.

Definitions:

Short Run

A period in which at least one factor of production is fixed, limiting the immediate capacity to adjust to changes in demand.

Long Run

A time frame where every production factor and cost can change, providing complete flexibility to adapt to new situations.

Short-Run Supply

The supply of goods that exists when producers are able to change the quantity of the good produced in response to changing prices, typically within a limited time frame.

Curve

A graphical representation of the relationship between two or more variables in a coordinate system, often used in economics to illustrate supply and demand.

Q27: Determine the percentage increase in sophomore 2.5

Q35: (time spent studying, percentage on exam)

Q56: What is the probability that a

Q64: 15, 7, 8, 19, 14, 13, 13,

Q72: Which is the best fertilizer for Mr.

Q74: The Director of Food Operations at a

Q109: The owner of a small manufacturing

Q114: 79, 25, 79, 13, 25, 29, 56,

Q143: An investigation of 150 randomly selected local

Q234: The permutation formula can be used