Use the information below to answer the following question.

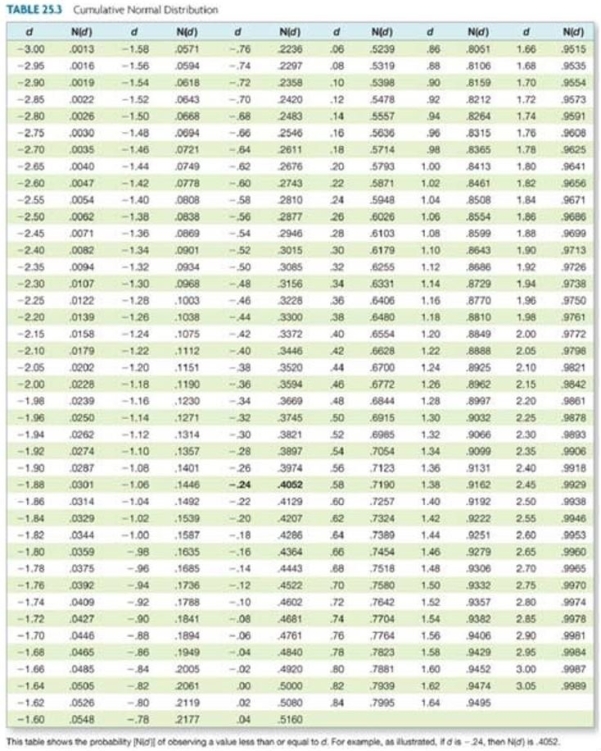

Assume a stock price of $88; risk-free rate of 4 percent per year, compounded continuously; time to maturity of five months; standard deviation of 48 percent per year; and a put and call exercise price of $85. What is the delta of the put option?

Definitions:

Photosynthesizing Bacteria

Microorganisms that convert light energy into chemical energy through the process of photosynthesis.

Terrestrial Plants

Plants that grow on land, as opposed to aquatic (water-based) or epiphytic (growing on other plants) plants.

Primitive Atmosphere

The early atmosphere of Earth, which was very different in composition from the current one, possibly composed of gases such as methane, ammonia, and water vapor.

Photosynthetic Bacteria

Bacteria that are capable of producing their own food through the process of photosynthesis.

Q9: AB Industries is an all-equity firm that

Q10: Product distribution and shelf placement do not

Q16: Assume the spot rate on the Japanese

Q37: A firm offers credit terms of 2/15,

Q40: Personal relevance is something that:<br>A) has an

Q49: Rosa purchased three call option contracts on

Q70: Frank's Auto can purchase new equipment for

Q71: The price of one euro expressed in

Q72: One reason why so many prices end

Q76: On Friday evening, Bank A loans Bank