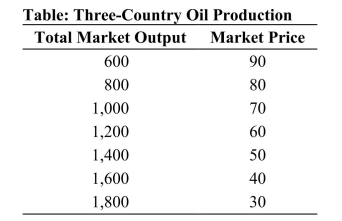

Reference: Ref 15-3 (Table: Three-Country Oil Production) Refer to the table. Suppose that three countries are engaged in oil production. For simplicity, assume zero costs so that revenue equals profit. Assume that Country A cheats on the cartel agreement by producing 200 more barrels than the other two countries. What is the new quantity sold by Country A?

Reference: Ref 15-3 (Table: Three-Country Oil Production) Refer to the table. Suppose that three countries are engaged in oil production. For simplicity, assume zero costs so that revenue equals profit. Assume that Country A cheats on the cartel agreement by producing 200 more barrels than the other two countries. What is the new quantity sold by Country A?

Definitions:

Long-Run Average Total Cost

The cost per unit of output incurred when all factors of production are variable, and scale of production can be changed.

Output

The amount of products or services produced by a company, industry, or economic system.

Total Fixed Cost

The sum of all costs that do not change with output level, including rent, salaries, and insurance.

Short Run

A period in economic analysis during which at least one input, such as plant size or capital, is fixed, limiting the ability to adjust to demand changes.

Q6: Which of the following statements is correct?<br>A)

Q13: <img src="https://d2lvgg3v3hfg70.cloudfront.net/TB3375/.jpg" alt=" Reference: Ref 14-6

Q22: When a policy is highly visible, appears

Q41: A monopolist's demand curve is described by

Q48: Economic profit differs from accounting profits because

Q93: Cartels do not last because their members

Q98: Which of the following is most likely

Q115: Charging each customer his or her maximum

Q122: Why are incentives so important in the

Q137: Government ownership of the media:<br>A) is uncommon