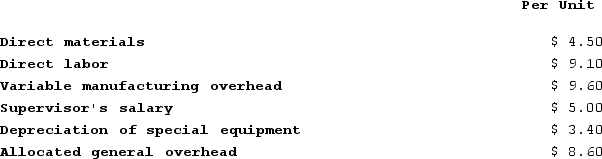

Part U16 is used by Mcvean Corporation to make one of its products. A total of 21,000 units of this part are produced and used every year. The company's Accounting Department reports the following costs of producing the part at this level of activity:  An outside supplier has offered to make the part and sell it to the company for $31.10 each. If this offer is accepted, the supervisor's salary and all of the variable costs, including the direct labor, can be avoided. The special equipment used to make the part was purchased many years ago and has no salvage value or other use. The allocated general overhead represents fixed costs of the entire company, none of which would be avoided if the part were purchased instead of produced internally. In addition, the space used to make part U16 could be used to make more of one of the company's other products, generating an additional segment margin of $33,000 per year for that product. The annual financial advantage (disadvantage) for the company as a result of buying part U16 from the outside supplier should be:

An outside supplier has offered to make the part and sell it to the company for $31.10 each. If this offer is accepted, the supervisor's salary and all of the variable costs, including the direct labor, can be avoided. The special equipment used to make the part was purchased many years ago and has no salvage value or other use. The allocated general overhead represents fixed costs of the entire company, none of which would be avoided if the part were purchased instead of produced internally. In addition, the space used to make part U16 could be used to make more of one of the company's other products, generating an additional segment margin of $33,000 per year for that product. The annual financial advantage (disadvantage) for the company as a result of buying part U16 from the outside supplier should be:

Definitions:

Q28: A balanced scorecard contains both customer and

Q62: Which of the following would be classified

Q99: In net present value analysis, the release

Q108: Wenner Corporation would like to use target

Q117: Norgaard Corporation makes 8,000 units of part

Q131: Alway Candy Corporation is implementing a target

Q148: Simkin Corporation keeps careful track of the

Q285: The management of Opray Corporation is considering

Q287: In the absorption approach to cost-plus pricing,

Q328: Holton Company makes three products in a