Use the following to answer questions:

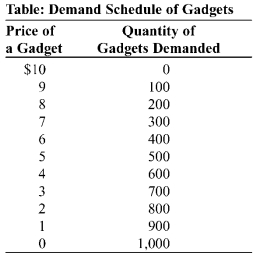

-(Table: Demand Schedule for Gadgets) Look at the table Demand Schedule for Gadgets. The market for gadgets consists of two producers, Margaret and Ray. Each firm can produce gadgets at a marginal cost of $2 and no fixed cost. Suppose that these two producers have formed a cartel, agreed to split production of output evenly, and are maximizing total industry profits. If Margaret decides to cheat on the agreement and sell 100 more gadgets, Margaret's price effect will be a(n) _____ in profit of _____.

Definitions:

Price

The sum of money needed to buy a product, service, or asset.

Long Run

A period in which all factors of production and costs are variable, allowing firms to adjust to changes in the market or economic conditions.

Demand

The quantity of a product or service that consumers are willing and able to buy at various prices during a specified period of time.

Industry Entry

The process of a new competitor or firm entering into an industry or market.

Q28: The demand curve for a monopoly is:<br>A)

Q53: Two large electronic retailers, Biggest Buy and

Q59: (Scenario: Payoff Matrix for Two Firms) In

Q82: Since a monopolistically competitive firm has the

Q144: Firms in the monopolistically competitive movie industry

Q150: The law enacted in 1890 to break

Q156: When farmers raise hogs, there are a

Q232: Which of the following describes a feature

Q255: A strategy that is the same regardless

Q294: Many hotel chains offer discounts to senior