Use the following to answer questions:

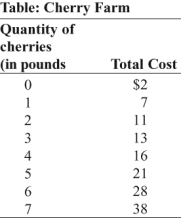

-(Table: Cherry Farm) Look at the table Cherry Farm. If Hank and Helen have one of 100 farms in the perfectly competitive cherry industry and if the price is $4, in the short run the industry will supply _____ pounds.

Definitions:

Fixed Costs

Costs that do not change with the level of production or sales, such as rent, salaries, and insurance premiums.

Marginal Cost Curve

A graphical representation that shows how the cost of producing one more unit of a good varies as production volume changes.

Diminishing Returns

A principle stating that as additional units of a variable input are added to a fixed input, the marginal product of the variable input eventually decreases.

Upward-Sloping

Describes a line or curve on a graph that moves higher on the y-axis as it moves to the right on the x-axis, typically used to describe a supply curve in economics.

Q43: (Table: Production of Bagels) Look at the

Q83: (Figure: The Profit-Maximizing Firm in the Short

Q120: If some firms in a perfectly competitive

Q121: Diminishing marginal returns occur when:<br>A) each additional

Q183: In a perfectly competitive market, tastes and

Q185: In the long run, when there are

Q218: A perfectly competitive firm's demand curve is

Q263: When Caroline's dress factory hires two workers,

Q337: (Table: Cakes) Look at the table Cakes.

Q345: (Table: Costs of Birthday Cakes) Look at