The following information relates to Questions

Serena Soto is a risk management specialist with Liability Protection advisors. trey hudgens, CFo of Kiest Manufacturing, enlists Soto's help with three projects. The first project is to defease some of Kiest's existing fixed-rate bonds that are maturing in each of the next three years. The bonds have no call or put provisions and pay interest annually. exhibit 1 presents the payment schedule for the bonds.

EXHIBIT 1 Kiest Manufacturing Bond Payment Schedule as of 1 October 2017

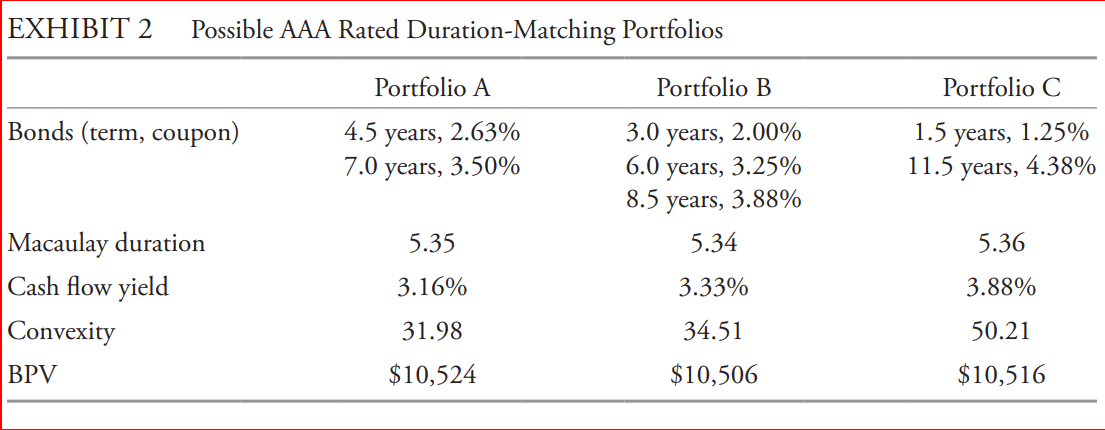

The second project for Soto is to help hudgens immunize a $20 million portfolio of liabilities. The liabilities range from 3.00 years to 8.50 years with a Macaulay duration of 5.34 years, cash flow yield of 3.25%, portfolio convexity of 33.05, and basis point value (bPv) of $10,505. Soto suggested employing a duration-matching strategy using one of the three aaa rated bond portfolios presented in exhibit 2.

Soto explains to hudgens that the underlying duration-matching strategy is based on the

Soto explains to hudgens that the underlying duration-matching strategy is based on the

following three assumptions.

1. yield curve shifts in the future will be parallel.

2. bond types and quality will closely match those of the liabilities.

3. The portfolio will be rebalanced by buying or selling bonds rather than using derivatives.

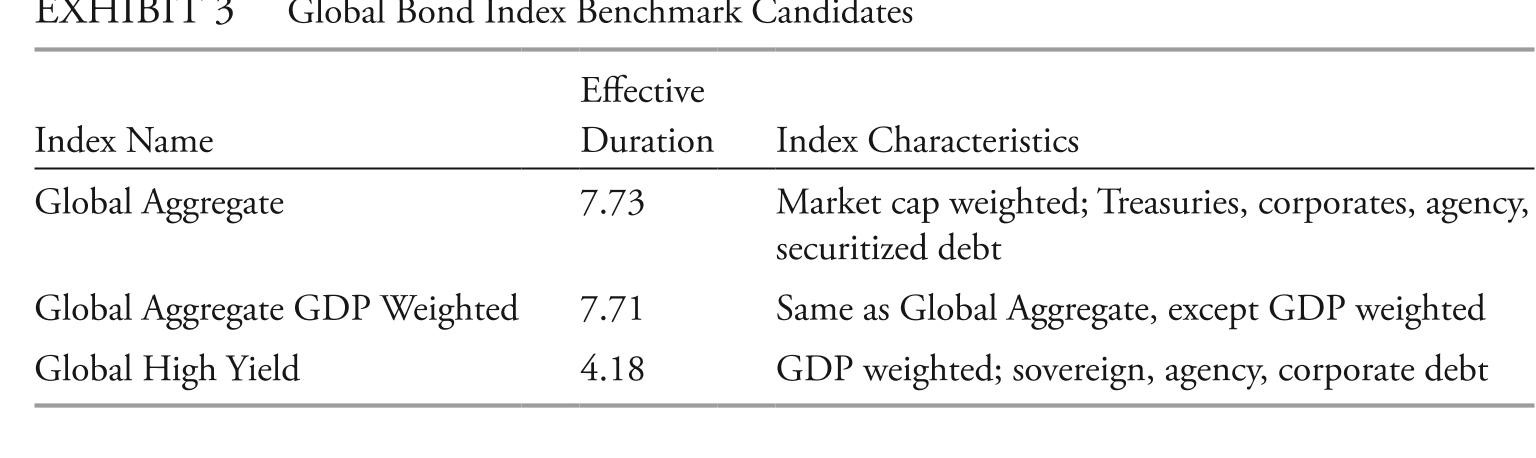

The third project for Soto is to make a significant direct investment in broadly diversified global bonds for Kiest's pension plan. Kiest has a young workforce, and thus, the plan has a long-term investment horizon. hudgens needs Soto's help to select a benchmark index that is appropriate for Kiest's young workforce and avoids the "bums" problem. Soto discusses three benchmark candidates, presented in exhibit 3.

With the benchmark selected, hudgens provides guidelines to Soto directing her to (1)

With the benchmark selected, hudgens provides guidelines to Soto directing her to (1)

use the most cost-effective method to track the benchmark and (2) provide low tracking error.after providing hudgens with advice on direct investment, Soto offered him additional information on alternative indirect investment strategies using (1) bond mutual funds, (2)

exchange-traded funds (etFs) , and (3) total return swaps. hudgens expresses interest in using bond mutual funds rather than the other strategies for the following reasons.

reason 1 total return swaps have much higher transaction costs and initial cash outlay than bond mutual funds.reason 2 Unlike bond mutual funds, bond etFs can trade at discounts to their underlying indexes, and those discounts can persist.reason 3 bond mutual funds can be traded throughout the day at the net asset value of the underlying bonds.

-Which of hudgens's reasons for choosing bond mutual funds as an investment vehicle is correct?

Definitions:

Jomo Kenyatta

A Kenyan anti-colonial activist and politician who became the first President of Kenya, playing a key role in the transition from British colonial rule to independence.

Security Council

A principal organ of the United Nations charged with maintaining international peace and security, comprising 15 member states, including five permanent members with veto power.

Veto Power

The right to unilaterally stop or reject a decision or proposal made by a law-making body, often held by a president, monarch, or other head of state.

Potsdam Conference

A summit held in 1945 where the leaders of the United States, the United Kingdom, and the Soviet Union met to negotiate terms for the end of World War II.

Q3: stepped steel shaft with diameters

Q5: The "second-order" effect on a bond's percentage

Q7: Which of the following factors in credit

Q12: based on exhibit 3, the implied australian

Q13: stepped steel shaft ( <span

Q14: based on Kowalski's assumptions and exhibits 2

Q14: Give the standard form of the

Q18: Which of the following sources of return

Q27: a bond has an annual modified duration

Q132: Evaluate the limit.<br> <span class="ql-formula" data-value="\lim