The following information relates to Questions

daniela ibarra is a senior analyst in the fixed-income department of a large wealth manage-ment firm. Marten Koning is a junior analyst in the same department, and david lok is a member of the credit research team.

The firm invests in a variety of bonds. ibarra is presently analyzing a set of bonds with some similar characteristics, such as four years until maturity and a par value of €1,000. exhibit 1 includes details of these bonds.

exhibit 1 a brief description of the bonds being analyzed bond descriptionb1 a zero-coupon, four-year corporate bond with a par value of €1,000. The wealth management firm's research team has estimated that the risk-neutral probability of default (the hazard rate) for each date for the bond is 1.50%, and the recovery rate is 30%.b2 a bond similar to b1, except that it has a fixed annual coupon rate of 6% paid annually.

b3 a bond similar to b2 but rated aa.

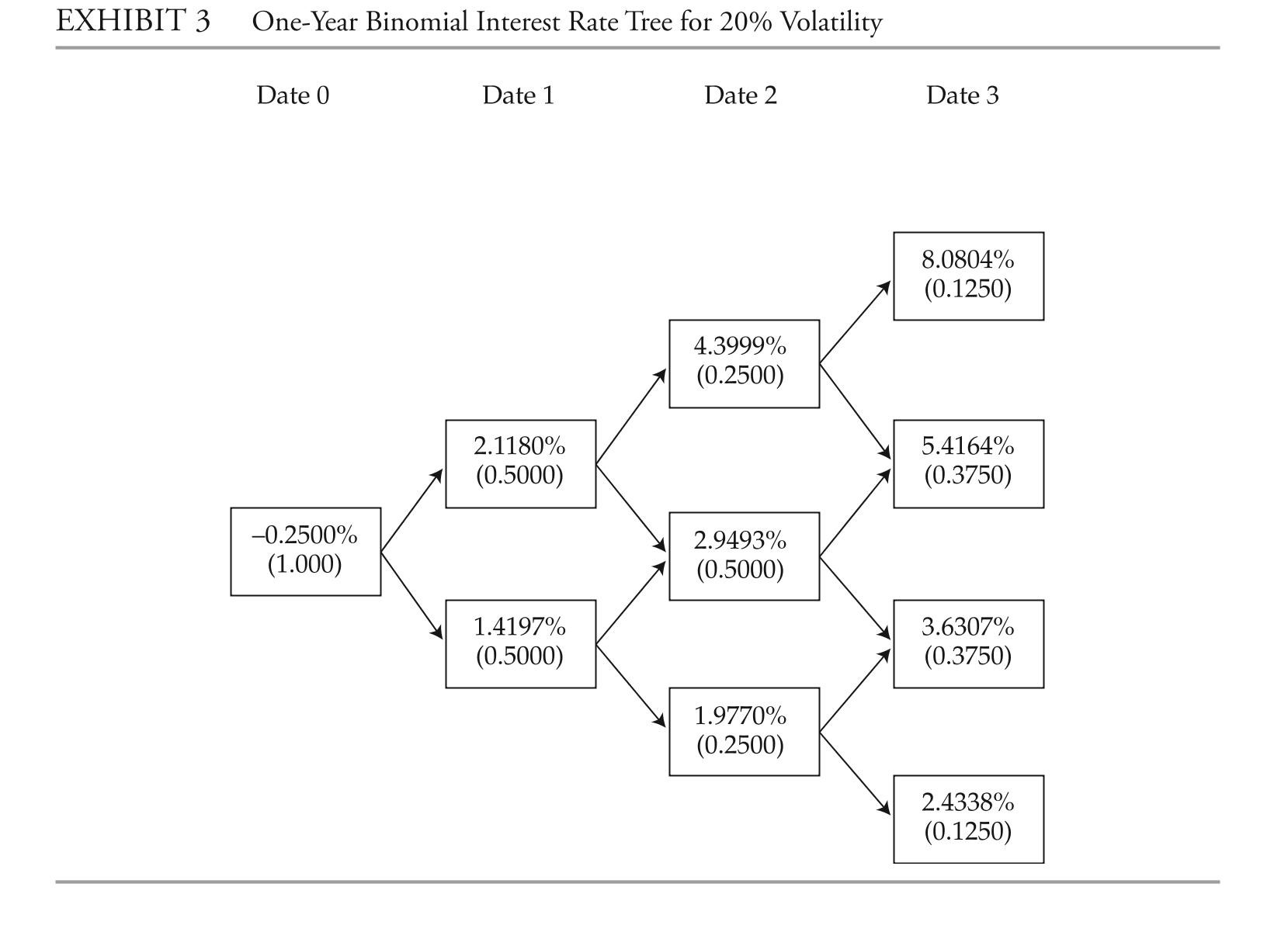

b4 a bond similar to b2 but the coupon rate is the one-year benchmark rate plus 4%.ibarra asks Koning to assist her with analyzing the bonds. She wants him to perform the analysis with the assumptions that there is no interest rate volatility and that the government bond yield curve is flat at 3%.ibarra performs the analysis assuming an upward-sloping yield curve and volatile interest rates. exhibit 2 provides the data on annual payment benchmark government bonds.1 She uses these data to construct a binomial interest rate tree (shown in exhibit 3) based on an assump-tion of future interest rate volatility of 20%.

1 For simplicity, this exhibit uses

answer the first five questions (1-4) based on the assumptions made by Marten Koning,the junior analyst. answer questions (8-12) based on the assumptions made by daniela ibarra, the senior analyst.

answer the first five questions (1-4) based on the assumptions made by Marten Koning,the junior analyst. answer questions (8-12) based on the assumptions made by daniela ibarra, the senior analyst.

Note: all calculations in this problem set are carried out on spreadsheets to preserve reci-sion. The rounded results are reported in the solutions.

-david lok has estimated the probability of default of bond b1 to be 1.50%. he is pre- senting the approach the research team used to estimate the probability of default. Which

Of the following statements is lok likely to make in his presentation if the team used a

Reduced-form credit model?

Definitions:

Neonatal Intensive Care

Neonatal Intensive Care is a specialized unit in a hospital that provides comprehensive care for newborns with health issues, premature birth, or requiring urgent medical attention.

Qigong

A Chinese discipline consisting of breathing and mental exercises combined with body movements.

Chiropractic Therapy

Treatment that focuses on the spine and its relation to the component bone structures, muscles, and nerves and treats a variety of symptoms through spinal manipulation or adjustment.

Respiratory Illnesses

Diseases that affect the air passages, including the nasal passages, the bronchi, and the lungs.

Q1: coefficient of friction between a block and

Q3: Two thin cables, each having a

Q7: based on the given Z-spreads for bonds

Q17: The value of Bond 3 is closest

Q24: If interest rates increase, an investor who

Q44: Select the graph of the polar

Q60: Select the graph of <span

Q76: Select the parametric equations matching with

Q77: Find the limit if <span

Q94: Suppose that the graph of is