Table 6-1

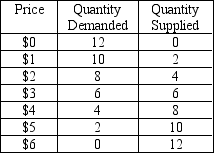

-Refer to Table 6-1.Suppose the government imposes a price ceiling of $5 on this market.What will be the size of the shortage in this market?

Definitions:

Barriers to Entry

Economic, procedural, regulatory, or technological factors that obstruct or limit the possibility of new competitors entering an industry.

Long-Run Equilibrium

A state in which all factors of production and costs are variable, allowing firms to make adjustments and the market to stabilize at a point where supply equals demand.

Competitive Market

A market structure characterized by many buyers and sellers, free entry and exit, and products that are close substitutes, leading to price competition.

Market Price

Market price is the price at which a good or service is bought and sold in the marketplace, determined by the forces of supply and demand.

Q53: If a 25% change in price results

Q75: If the income elasticity of demand for

Q138: A result of welfare economics is that

Q148: If a price ceiling is a binding

Q158: The price elasticity of demand is defined

Q349: Welfare economics is the study of<br>A) the

Q372: The long-run effects of rent controls are

Q412: How does total revenue change as one

Q432: If a tax is imposed on the

Q448: Suppose that the demand for lava lamps