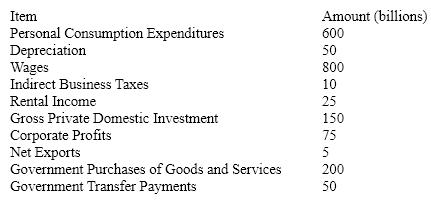

Table 8-1  According to the data in Table 8-1, the value of NNP is

According to the data in Table 8-1, the value of NNP is

Definitions:

Long Run

A period in economics where all factors of production and costs are variable, allowing companies to adjust to new conditions.

Average Total Cost

The total cost of production (fixed and variable costs combined) divided by the total quantity produced, indicating the cost per unit of product.

Marginal Revenue

The additional income received from selling one more unit of a good or service.

Industry Supply Curve

A graphical representation showing the total quantity of a good or service that producers in an industry are willing and able to supply at different price levels.

Q6: If the MPC of an economy is

Q19: Compared to the 1948 - 1973 period,

Q22: Increases in the supply of scientists and

Q49: The underlying cause of inflation is<br>A) labor

Q57: A constant contributor to labor productivity growth

Q82: In 2010, in order to stimulate capital

Q124: Identify the "oversimplified multiplier formula."<br>A) Multiplier =

Q198: If the multiplier is 4 and real

Q211: Government-produced goods are added to GDP at<br>A)

Q217: How is human capital most commonly measured?<br>A)