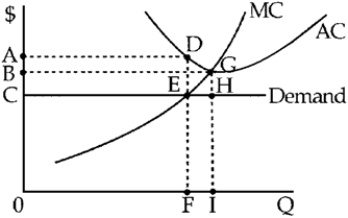

Figure 10-2

-In the short run, perfectly competitive firms will determine whether to continue producing the current output, reduce output, or increase output based on the relationship between

Definitions:

Marginal Cost Function

A mathematical representation showing how the cost of producing one additional unit of a good changes as production volume changes.

Optimal Output

The level of production that maximizes a firm’s profit or minimizes its cost under given conditions.

Profit

The financial gain acquired when the revenue generated from business activities exceeds the expenses, costs, and taxes needed to sustain the activity.

Industry Supply Curve

A graph that shows the relationship between the price of a good and the total output of the industry for that good.

Q20: The supply curve for a perfectly competitive

Q35: Since a monopolist has a unique product,

Q63: At a firm's profit-maximizing level of output,

Q104: Figure 10-1 <br><img src="https://d2lvgg3v3hfg70.cloudfront.net/TBX9061/.jpg" alt="Figure 10-1

Q112: A corporation's income is taxed<br>A)immediately after it

Q155: Double taxation is a problem for corporations.

Q189: The market demand curve in perfect competition

Q209: The necessity for choice, in economics, arises

Q215: The assignment of inputs to specific industries

Q231: Under the theory of perfect competition, firms