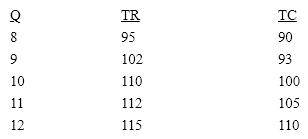

Table 11-2  In Table 11-2, marginal revenue at the profit-maximizing output is how much?

In Table 11-2, marginal revenue at the profit-maximizing output is how much?

Definitions:

Long Run

A timeframe during which all production factors and expenses can change, permitting adjustments to all inputs.

Allocative Efficiency

A state of the economy in which production is in accordance with consumer preferences; every good or service is produced up to the point where the last unit provides a utility to consumers equal to the cost of producing it.

Consumer Surplus

The difference in the amount consumers are prepared and have the means to pay for a service or good compared to the amount they actually do pay.

Producer Surplus

The difference between what producers are willing to accept for a good versus what they actually receive, often depicted as the area above the supply curve and below the market price.

Q9: The marginal revenue curve for a monopolist

Q87: Table 11-1 <img src="https://d2lvgg3v3hfg70.cloudfront.net/TBX9061/.jpg" alt="Table 11-1

Q103: The monopolistically competitive firm differs from monopoly

Q112: Economies of scale imply: (i)a continuously falling

Q163: A monopolist is a price maker.

Q172: In a planned economy, the concept of

Q205: What is true for both a monopolist

Q212: Using prices to promote efficiency in the

Q236: The key element in preserving a monopoly

Q247: If a technological breakthrough reduces input quantities