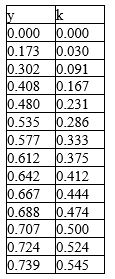

Suppose an economy uses only two inputs in production: capital and labour. The following table describes a production function, where y stands for output per worker and k is capital per worker.

a) Draw approximately this production function with y on the vertical axis.

b) Show that this production function exhibits diminishing returns to scale.

c) Suppose there are two countries, A and B. The economies of the two countries can be described by this production function. If Country A has initially a capital-labour ratio k = 0.167 and Country B has k = 0.412, show that an equal increase in capital produces more extra output in country A than in Country B.

Definitions:

Corresponding Cost

Corresponding cost refers to the specific expenses directly associated with the production of a good or service, similar to direct costs.

Discount Period

The time frame in which a payment can be made at a discounted rate from the total amount owed.

Perpetual

An inventory system where updates are made continuously to the inventory records, reflecting each sale or purchase.

Periodic Inventory System

An inventory system in which the inventory count and the cost of goods sold calculation are performed at set intervals, typically at the end of an accounting period.

Q12: What led to the decrease in labour-force

Q23: (Challenging) Draw a firm's labour demand curve

Q36: Which statement best defines "indexation"?<br>A) It is

Q62: Yohanna, the CEO of a corporation operating

Q66: Refer to the Figure 9-1. If there

Q94: When unions raise wages in some sectors

Q114: How is the unemployment rate computed?<br>A) by

Q118: Suppose a bank has $10,000 in deposits

Q139: How does M1 compare with M2?<br>A) M1+

Q175: Corporations receive no proceeds from the resale