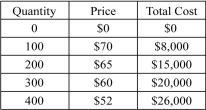

The following table shows a firm's total cost of producing different quantities of output and the price that consumers are willing to pay for those quantities of the good.

a)If the firm is monopolistically competitive,what is the equilibrium output for the firm?

b)What is the equilibrium price charged by the firm?

c)Calculate the profit earned or the loss incurred by the firm in the short run.

Definitions:

Consequences

The outcomes or effects that stem from a particular action or decision, which can be intended or unintended and positive or negative.

Stability

The condition of an economy characterized by constant or predictable levels of growth, inflation, and employment.

Steady Rate

A constant or unchanging rate over a period of time, often used to describe economic growth, inflation, or other financial metrics.

Economic Growth

An increase in the production of goods and services in an economy over time, often measured by the rise in Gross Domestic Product (GDP).

Q41: Which of the following is most likely

Q47: Refer to the scenario above.Does Mello Yello

Q61: Norah works as a content writer for

Q63: There are two major Internet service providers

Q89: Refer to the scenario above.This game _.<br>A)

Q94: In a zero-sum game,_.<br>A) each player earns

Q123: Which of the following is a difference

Q169: Refer to the scenario above.What is likely

Q235: In practice,price discrimination is never perfect.Why?

Q247: Refer to the figure above.Compared to the