Figure 13.3

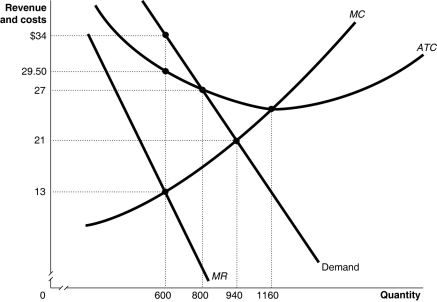

Figure 13.3 shows the demand and cost curves for a monopolist.

-Refer to Figure 13.3.What is the amount of the monopoly's total cost of production?

Definitions:

Quantity Supplied

The total amount of a good or service that producers are willing and able to sell at a given price over a specific period.

Quantity Demanded

The aggregate quantity of a product or service that buyers are prepared and capable of buying at a certain price point.

Equilibrium Price

The cost at which the amount of a product or service that consumers want to buy matches the amount that producers are willing to sell, creating a balanced market situation.

Demand

The quantity of a product or service that consumers are willing and able to purchase at various price levels, at a given point in time.

Q24: Customer discrimination occurs when<br>A)a firm pays workers

Q29: If an industry is made up of

Q54: Users fees for ports and marinas are

Q57: What is the difference between a marginal

Q78: The National Hockey League has long-term leases

Q82: Which of the following is an example

Q87: Firms in perfect competition produce the productively

Q124: Which of the following is not true

Q133: Refer to Figure 15.1.The excess burden of

Q138: Refer to Figure 11.6.What is the monopolistic