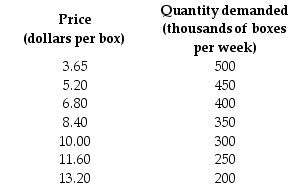

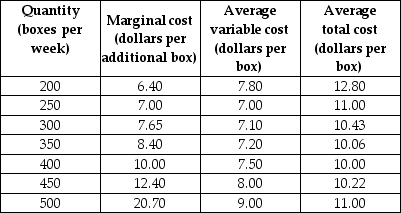

Use the table below to answer the following question.

Table 12.2.4

-Refer to Table 12.2.4. The market is perfectly competitive and there are 1,000 firms that produce paper. The top table sets out the market demand schedule for paper.

Each producer of paper has the costs shown in the bottom table when it uses its least-cost plant size.

The market price is ________ a box and the market output is ________ boxes. The output produced by each firm is ________ boxes. Each firm ________.

Definitions:

Equilibrium Quantity

The amount of products or services available and sought after at the balance price in a marketplace.

Demand

The quantity of a product or service that consumers are willing and able to purchase at a given price.

Equilibrium Price

The market price at which the quantity of a good or service demanded by consumers equals the quantity supplied by producers.

Equilibrium Quantity

The level of goods or services being both offered and requested at the market's equilibrium price.

Q11: "The rich should face higher income tax

Q19: Refer to Figure 12.2.2, which shows a

Q33: The distinguishing features of oligopoly are _

Q39: The short run is a time frame

Q62: Suppose in an industry a firm realizes

Q65: Table 15.2.2 gives the payoff matrix in

Q87: Firms coordinate economic activity more efficiently than

Q98: If firms exit an market, the<br>A)market supply

Q175: Which of the following would an economist

Q177: Given the data in Table 1A.4.1, holding