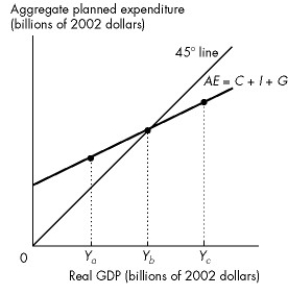

Use the figure below to answer the following questions.

Figure 27.2.1

There are no exports or imports in this economy.

-Refer to Figure 27.2.1. When real GDP is equal to Yb, then

Definitions:

Productive Efficiency

A state where goods are produced at the lowest possible cost, utilizing resources effectively without waste.

Average Total Cost

The total cost of production (fixed and variable costs combined) divided by the number of units produced, showing the cost per unit of output.

Short-run Equilibrium

A state in an economy or market where supply equals demand, considering that some factors (like capital) are fixed in the short term.

Decreasing-cost Industry

An industry characterized by a reduction in average costs as the scale of production increases, usually due to factors like technological advances.

Q18: Which one of the following factors will

Q18: Refer to Figure 28.2.2. If the short-run

Q27: Point A in Figure 3.2.1 indicates that<br>A)$1

Q29: Consider Fact 24.1.2. M1 is<br>A)$57 billion.<br>B)$268 billion.<br>C)$431

Q36: The Ricardo-Barro effect holds that<br>A)equal increases in

Q37: At the end of 2011, the government

Q60: An increase in income<br>A)increases the demand for

Q68: The factor leading to business cycles in

Q79: The economy is in a recession and

Q96: In Figure 27.3.2, the multiplier is<br>A)0.25.<br>B)1.00.<br>C)1.60.<br>D)2.50.<br>E)10.