Based on the company and its environment,including its internal control,the auditors assessed the risk of material misstatements to the financial statements,whether due to error or fraud,and designed the nature,timing,and extent of further audit procedures to be performed.

As a result of conducting the above risk assessment procedures,the audit plan for year 2 includes the following changes from the audit plan for year 1.The company has a calendar year-end and operates only on weekdays.

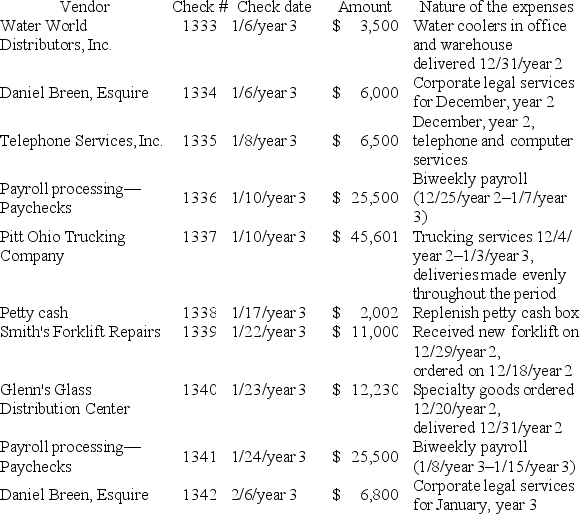

In conducting the audit procedures for the search for unrecorded liabilities,the materiality/scope for this area was assessed by the auditors at $6,000.Adjustments are only recorded for items equal to,or exceeding materiality.The last day of fieldwork is estimated to be February 1,year 3.

For the items reflected in the following check register,which are not recorded in the accounts payable subsidiary ledger at December 31,year 2,determine if each potential liability is recorded in the proper accounting period and also determine the amount that should be journalized,if any.If no action is required,you must enter $0.

For each of the check numbers in the table below,select if any action or adjustment is required. If no action is required,put $0 in the amount column;if an adjustment is needed select the dollar amount.Each selection may be used once,more than once,or not at all.

Check Register

Definitions:

Standardization

Establishing norms for comparing the scores of people who will take a test in the future; administering tests using a prescribed procedure.

Reliability

The extent to which a measure is consistent and free from error, providing similar results under consistent conditions.

IQ Scores

A measure of a person's cognitive abilities and potential, commonly expressed as a score derived from standardized tests designed to assess human intelligence.

Percentage

A mathematical term describing a number or ratio expressed as a fraction of 100.

Q13: According to PCAOB standards for reporting on

Q13: In governmental accounting,emphasis is placed on:<br>A)Total assets

Q15: When an auditor does <b>not</b> confirm material

Q17: An auditor plans to examine a sample

Q18: Which must management communicate to the

Q29: When control risk for the existence assertion

Q35: Registered bondholders receive periodic interest payments without

Q35: When there is substantial doubt about a

Q44: The party responsible for assumptions identified in

Q55: Operating control over check signing normally should