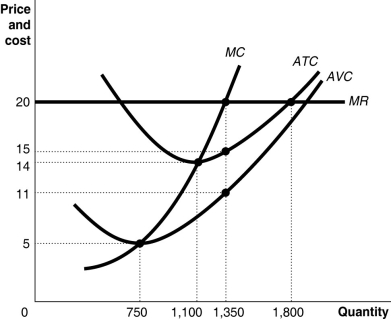

Figure 9-11

-Refer to Figure 9-11.If this is a constant-cost industry,what is the market price in the long-run equilibrium?

Definitions:

Units Produced

The total quantity of products manufactured or produced by a company or an industry within a specific period.

Variable Cost Function

A mathematical representation of the variable costs incurred by a firm, showing how these costs change with the level of output.

Marginal Cost Curve

A graphical representation of the change in total production costs with respect to the change in the quantity produced.

Constant

A fixed value that does not change in mathematical equations or scientific experiments, often representing fundamental principles or conditions.

Q20: If a firm is a natural monopoly,competition

Q69: A perfectly competitive firm in a constant-cost

Q91: Refer to Figure 9-5.If the market price

Q96: Suppose the total cost of producing 40,000

Q154: A wheat farmer and a firm in

Q169: Which of the following statements is true?<br>A)

Q216: Assume that you observe the long-run average

Q217: Which of the following statements is consistent

Q239: In the long run<br>A) the firm's fixed

Q246: A firm's short-run average total cost curve