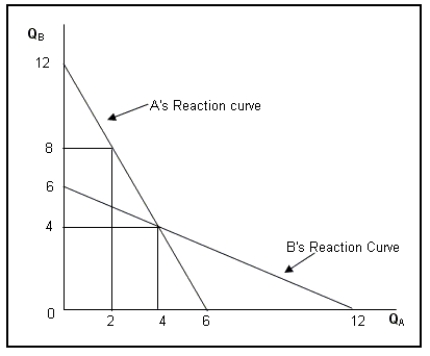

The figure given below represents the output choices of each of the two oligopolists, given the choices of its competitor.QA and QB are the quantities of output produced by Producer A and Producer B.The marginal cost of production is zero for both producers.

-Refer to Figure .If the two producers agree to act as a single monopoly firm, what will be the total output produced in the economy?

Definitions:

Labour Cost

The total expense incurred for hiring employees, including wages, benefits, and taxes.

Labour Efficiency Variance

A cost management tool used to measure the difference between the actual labor hours used and the standard labor hours expected to produce a certain level of output.

Direct Labour Standard

A benchmark for the amount of work (measured in labor hours or costs) expected to produce a certain quantity of goods.

Uncontrollable Costs

Costs that cannot be influenced or controlled by a manager under normal circumstances.

Q2: The board of directors of Fast Food

Q5: An insurance policy is a contract that:<br>A)benefits

Q9: Burkes Inc.should stop production in the short

Q15: An information is beneficial to the decision-maker

Q17: If the costs of negotiating and enforcing

Q18: A packaged fruit juice manufacturer contracts with

Q40: When people use a recognition heuristic, they

Q52: With cheaper communication technology and easy flow

Q52: What is deadweight loss?<br>A)It is the amount

Q64: Which of the following factors can delay