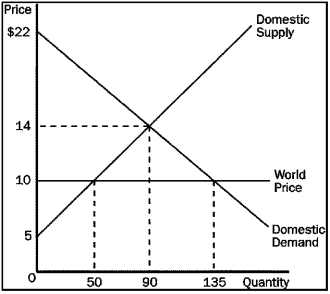

Using the graph below, answer the following questions about hammers.

a. What is the equilibrium price of hammers before trade?

b. What is the equilibrium quantity of hammers before trade?

c. What is the price of hammers after trade is allowed?

d. What is the quantity of hammers imported after trade is allowed?

e. What is the amount of consumer surplus before trade?

f. What is the amount of consumer surplus after trade?

g. What is the amount of producer surplus before trade?

h. What is the amount of producer surplus after trade?

i. What is the amount of total surplus before trade?

j. What is the amount of total surplus after trade?

k. What is the change in total surplus because of trade?

Definitions:

Technology Advances

Progressive developments and improvements in technology that enhance productivity, efficiency, and the quality of goods and services.

Production Possibilities Curve

A graph that shows the maximum quantity of one good that can be produced for each possible quantity of another good produced, illustrating the trade-offs and opportunity costs of production choices.

Inefficiently

A descriptor for processes or activities that do not use resources in the best possible way, resulting in wasted effort or energy and not achieving maximum productivity.

Economic Growth

Economic growth refers to an increase in the productive capacity of an economy, evidenced by a rise in national income, goods, and services over a period of time.

Q10: In the United States in 2009, consumption

Q119: In the economy of Ukzten in 2010,

Q178: Refer to Table 10-1. What were country

Q188: What basket of goods and services is

Q202: Economists feel that national security concerns never

Q252: Which of the following statements is true?<br>A)Free

Q324: Refer to Table 10-6. In 2008, this

Q324: Refer to Figure 9-16. Government revenue raised

Q333: U.S. real GDP is substantially higher today

Q409: Which of the following is not a