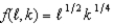

Suppose all firms in a perfectly competitive industry have production processes characterized by the production function  .Suppose the cost of labor is 20 and the cost of capital is 10.

.Suppose the cost of labor is 20 and the cost of capital is 10.

a.Suppose that the industry is in long run equilibrium and that firms are using 1 unit of capital.What is the short run cost function of each firm?

b.Suppose there are 5,000 firms in long run equilibrium.What is the short run market supply function?

c.Suppose market demand is  What is the equilibrium price?

What is the equilibrium price?

d.Firms in this industry face a recurring fixed cost FC.What must FC be in order for this industry to indeed be in long run equilibrium with its 100 firms?

Definitions:

Continuous Budget

A rolling budget for a 12-month period where the budget moves forward one month (or another period) as the current month (or period) is completed.

Perpetual Budget

A continuously updated budget that adjusts and rolls over to subsequent periods as the financial year progresses.

Rolls Forward

A term used in accounting to describe the process of moving figures from one period to the next, often related to budgets or forecasts.

Budgets

Financial plans that outline expected revenues and expenditures for a specific period, guiding spending and investment decisions.

Q1: In the one-input model, a convex producer

Q2: The budget line on a graph represents

Q8: Price ceilings have to be set above

Q16: In our study of monopoly, we found

Q17: Unless goods are Giffen goods, own-price elasticities

Q20: Suppose that, at a given production plan,

Q26: Briefly describe how the ultracentrifuge is used

Q27: Regardless of how price inelastic the supply

Q28: Suppose a single-input production function has initially

Q72: Market segmentation efforts, target marketing, and brand